In today's rapidly changing economic landscape, understanding the escalation clause in insurance has become more important than ever. This clause plays a crucial role in protecting policyholders from unforeseen increases in costs due to inflation or other economic factors. Whether you're a business owner or an individual seeking financial security, knowing how this clause works can significantly impact your financial planning and protection.

Insurance policies are designed to provide financial security and peace of mind, but they must also adapt to changing economic conditions. The escalation clause ensures that the coverage remains relevant and effective even as costs rise over time. This article will delve into the details of this important clause and explain its implications for both policyholders and insurers.

By the end of this guide, you'll have a clear understanding of what the escalation clause in insurance entails, how it benefits you, and how to incorporate it into your insurance strategy. Let's begin by exploring the basics of this crucial component of modern insurance policies.

Read also:Discovering The World Of Actress S A Comprehensive Guide

Table of Contents

- What is Escalation Clause in Insurance?

- History and Importance of Escalation Clause

- Types of Escalation Clauses

- Benefits of Escalation Clauses

- Key Components of an Escalation Clause

- How Escalation Clause Works in Insurance

- Examples of Escalation Clause in Real-Life Scenarios

- Common Misconceptions About Escalation Clause

- Legal Considerations and Regulations

- Conclusion and Next Steps

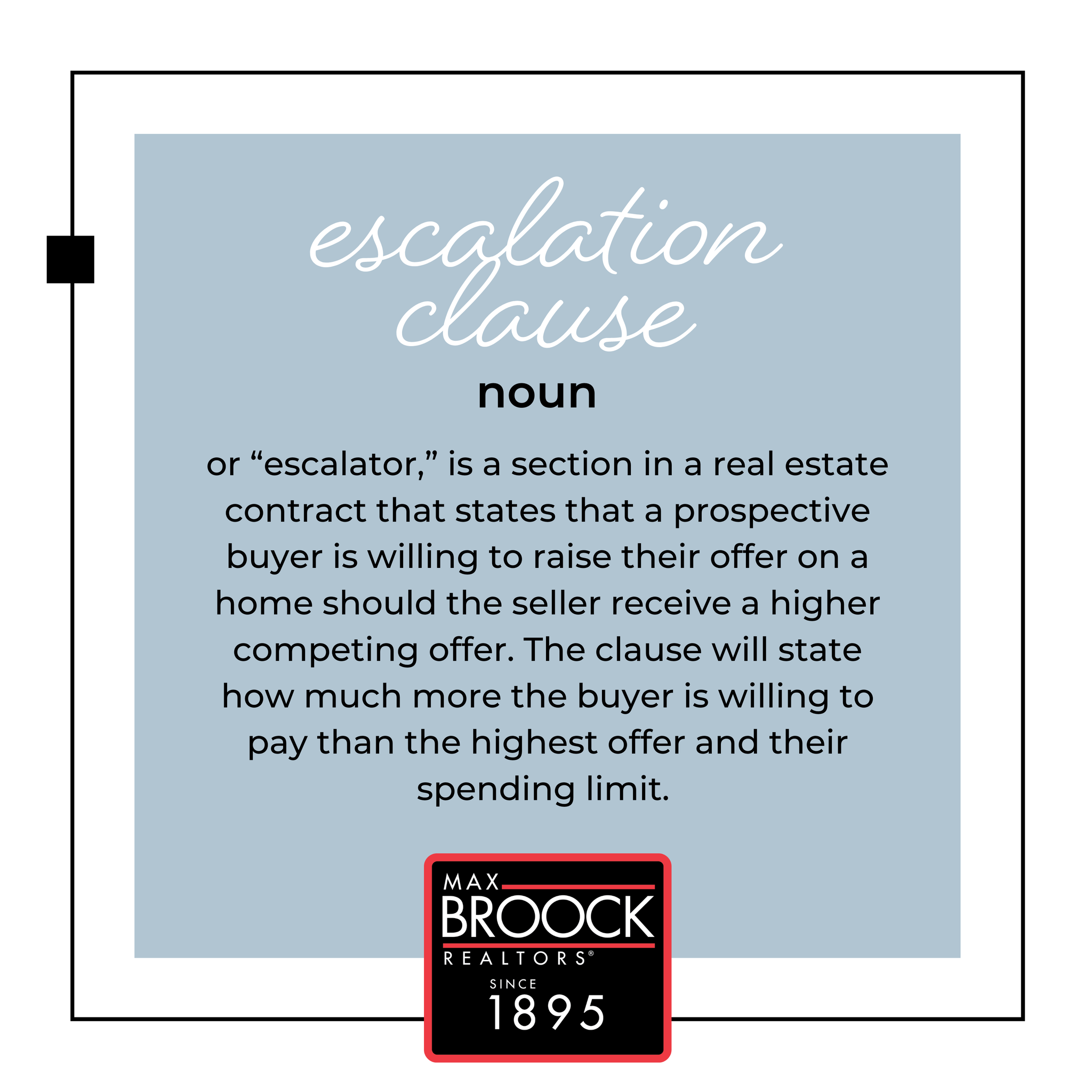

What is Escalation Clause in Insurance?

An escalation clause in insurance refers to a provision included in a policy that allows for automatic adjustments to coverage limits or premiums based on predefined economic factors. This clause is particularly useful in policies where the cost of covered items, such as property or medical expenses, is subject to inflation or other economic fluctuations.

This mechanism ensures that the policy remains relevant and effective over time, protecting both the insurer and the policyholder from unexpected financial burdens. By incorporating an escalation clause, insurers can offer more flexible and adaptable coverage options that align with real-world economic conditions.

Why is Escalation Clause Necessary?

The necessity of an escalation clause stems from the unpredictable nature of economic environments. For instance, inflation can significantly increase the cost of rebuilding a property or obtaining medical treatment. Without an escalation clause, policyholders may find themselves underinsured, leading to potential financial losses.

History and Importance of Escalation Clause

The concept of the escalation clause in insurance has evolved over the years in response to changing economic conditions. Historically, insurance policies were designed with fixed limits, which often proved insufficient during periods of high inflation or economic instability.

As economic conditions became more volatile, insurers and policyholders recognized the need for a mechanism that could adapt to these changes. This led to the development of the escalation clause, which has since become an integral part of many modern insurance policies.

Importance in Modern Insurance

In today's dynamic economic environment, the importance of the escalation clause cannot be overstated. It serves as a safeguard against unforeseen economic shifts, ensuring that policyholders remain adequately covered regardless of external factors.

Read also:Discover Marlboro High School A Hub Of Excellence And Growth

Types of Escalation Clauses

There are several types of escalation clauses, each tailored to specific types of insurance policies and economic conditions. Understanding these variations is essential for selecting the right clause for your needs.

1. Indexed Escalation Clause

This type of clause adjusts coverage limits based on a specific economic index, such as the Consumer Price Index (CPI). It provides a straightforward and transparent method for adjusting coverage in line with inflation.

2. Fixed Percentage Escalation Clause

With a fixed percentage escalation clause, coverage limits increase by a predetermined percentage each year. This approach offers predictable adjustments and is often used in policies where inflation rates are relatively stable.

Benefits of Escalation Clauses

Incorporating an escalation clause in your insurance policy offers numerous benefits, including:

- Increased Coverage Protection: Ensures that coverage limits remain relevant even as costs rise.

- Financial Stability: Provides peace of mind by protecting against unexpected increases in costs.

- Flexibility: Allows for adjustments based on economic conditions, making policies more adaptable.

Key Components of an Escalation Clause

Every escalation clause consists of several key components that define its functionality and effectiveness. These include:

- Trigger Mechanism: The specific economic factor or index that triggers the adjustment.

- Adjustment Frequency: How often the clause is applied, typically annually or semi-annually.

- Limitations: Any caps or restrictions on the extent of the adjustments.

How These Components Work Together

The interplay of these components ensures that the escalation clause operates effectively, balancing the needs of both insurers and policyholders. By clearly defining these elements, insurers can offer transparent and reliable coverage options.

How Escalation Clause Works in Insurance

The operation of an escalation clause involves monitoring predefined economic indicators and applying adjustments to coverage limits or premiums accordingly. This process is typically automated, ensuring timely and accurate updates.

Step-by-Step Process

- Monitor the specified economic index or factor.

- Calculate the required adjustment based on the observed changes.

- Apply the adjustment to the policyholder's coverage limits or premiums.

Examples of Escalation Clause in Real-Life Scenarios

Real-life examples illustrate the practical application and benefits of escalation clauses in various insurance contexts:

Example 1: Property Insurance

Consider a homeowner with a property insurance policy that includes an escalation clause tied to the CPI. Over time, as construction costs rise due to inflation, the policy automatically adjusts the coverage limit to ensure the homeowner remains adequately insured.

Example 2: Health Insurance

In health insurance, an escalation clause may adjust coverage limits based on rising medical costs. This ensures that policyholders can afford necessary treatments without incurring additional expenses.

Common Misconceptions About Escalation Clause

Despite its benefits, there are several misconceptions surrounding the escalation clause:

- Misconception 1: It increases premiums excessively.

- Misconception 2: It only benefits insurers.

Addressing these misconceptions is crucial for fostering a better understanding of the clause's true value.

Legal Considerations and Regulations

The implementation of escalation clauses is subject to various legal considerations and regulations. Insurers must ensure compliance with local laws and regulations to avoid potential legal issues.

Key Legal Requirements

Some key legal requirements include:

- Transparent disclosure of clause details in policy documents.

- Adherence to specified adjustment methodologies.

Conclusion and Next Steps

In conclusion, the escalation clause in insurance is a vital tool for ensuring comprehensive and adaptable coverage in an ever-changing economic landscape. By understanding its function, benefits, and legal considerations, policyholders can make informed decisions about incorporating this clause into their insurance strategies.

We encourage you to take action by reviewing your current policies and considering the inclusion of an escalation clause. Feel free to share this article with others who may benefit from this knowledge and explore more resources on our website for further insights into insurance and financial planning.